DC Circuit: Tax Court was Wrong; IRS has the Authority To Assess Form 5471 Penalties

Summary

On Friday, May 3, 2024, the U.S. Circuit Court for the D.C. Circuit overturned the Tax Court’s decision in Farhy v. Commissioner, ___ F.4th ___ (D.C. Cir. 5/3/24) (link to opinion) and held that the IRS has authority under § 6038(b) to assess Form 5471 penalties.

The Tax Court previously held that the Internal Revenue Code (IRC or the “Code”) (specifically § 6038(b)) did not grant the IRS authority to “assess” Form 5471 penalties. Instead, the Tax Court concluded that the IRS needed to bring a federal district court suit to reduce the amount to judgment before collecting the penalty.

The D.C. Circuit rejected this analysis and held that “the text, structure, and function of section 6038 demonstrate that Congress authorized assessment of penalties imposed under subsection (b).” Therefore, the D.C. Circuit held that the IRS had the authority to assess the penalty and proceed with the collection of the penalties.

This may not be the end of the line for the Farhy case. A three-judge panel issued the opinion so the taxpayer could request a rehearing en banc. Alternatively, the taxpayer could file a writ of certiorari to the U.S. Supreme Court.

For other taxpayers, how the U.S. Tax Court will react to the D.C. Circuit’s decision remains to be seen. Under the Golsen rule, the Tax Court is bound to apply the D.C. Circuit’s holding to cases that are appealable to the D.C. Circuit. However, for all other taxpayers, the Tax Court is not bound to the D.C. Circuit’s holding. In these cases, the Tax Court could continue to apply its holding or choose to follow the D.C. Circuit’s holding and overturn its prior decision.

Why Farhy Matters: Procedural Importance of Authority to Assess Form 5471 Penalties

An assessment is simply a bookkeeping entry noting that a taxpayer owes the U.S. government a debt for tax, penalties, and interest under the Code. Although it is simple, entering the assessment is extremely important because it marks the point in time at which the IRS can begin to utilize its powerful lien and levy powers to collect the debt.

For most types of assessments, the taxpayer has preassessment rights to challenge a proposed assessment. For example, suppose the IRS proposes to increase the amount a taxpayer owes after an examination. In that case, the taxpayer usually has administrative rights to challenge the proposed assessment through a hearing with IRS Appeals. Alternatively, the taxpayer has a statutory right to petition the U.S. Tax Court to challenge the proposed assessment. Until these rights have lapsed or been exhausted, the IRS cannot collect the proposed assessment.

However, there are no preassessment rights for some types of penalties called assessable penalties. Instead, the IRS is allowed to assess the penalty and begin collection action. In these cases, the taxpayer is generally provided administrative rights to a hearing with IRS Appeals. Alternatively, the taxpayer can pay the assessment and challenge the merits of the penalty by filing a refund claim. Then, assuming the IRS denies the claim, the taxpayer can file a refund suit in federal district court.

Form 5471 penalties have long been considered an assessable penalty. However, as discussed below, the Tax Court held in Farhy that the IRS doesn’t have the authority to assess Form 5471 penalties.

On Friday, May 3, 2024, the D.C. Circuit held that the IRS does have authority to assess Form 5471 penalties.

Overview of Tax Court Case & D.C. Circuit’s Holding

Quick Summary of Taxpayer’s Facts

The taxpayer was a U.S. permanent resident for the years in question (2003 through 2010). He resided in Israel when he petitioned the U.S. Tax Court and when the IRS appealed to the D.C. Circuit.

During his 2003 through 2010 taxable years (years at issue), the taxpayer was the sole owner of a foreign corporation incorporated in Belize. He was also the sole owner from 2005 (at the latest) through 2010; the taxpayer also owned another foreign corporation incorporated in Belize. These entities were established as part of an illegal scheme to reduce the amount of income tax that he owed. The taxpayer cooperated with authorities, so he was granted immunity from prosecution.[1]

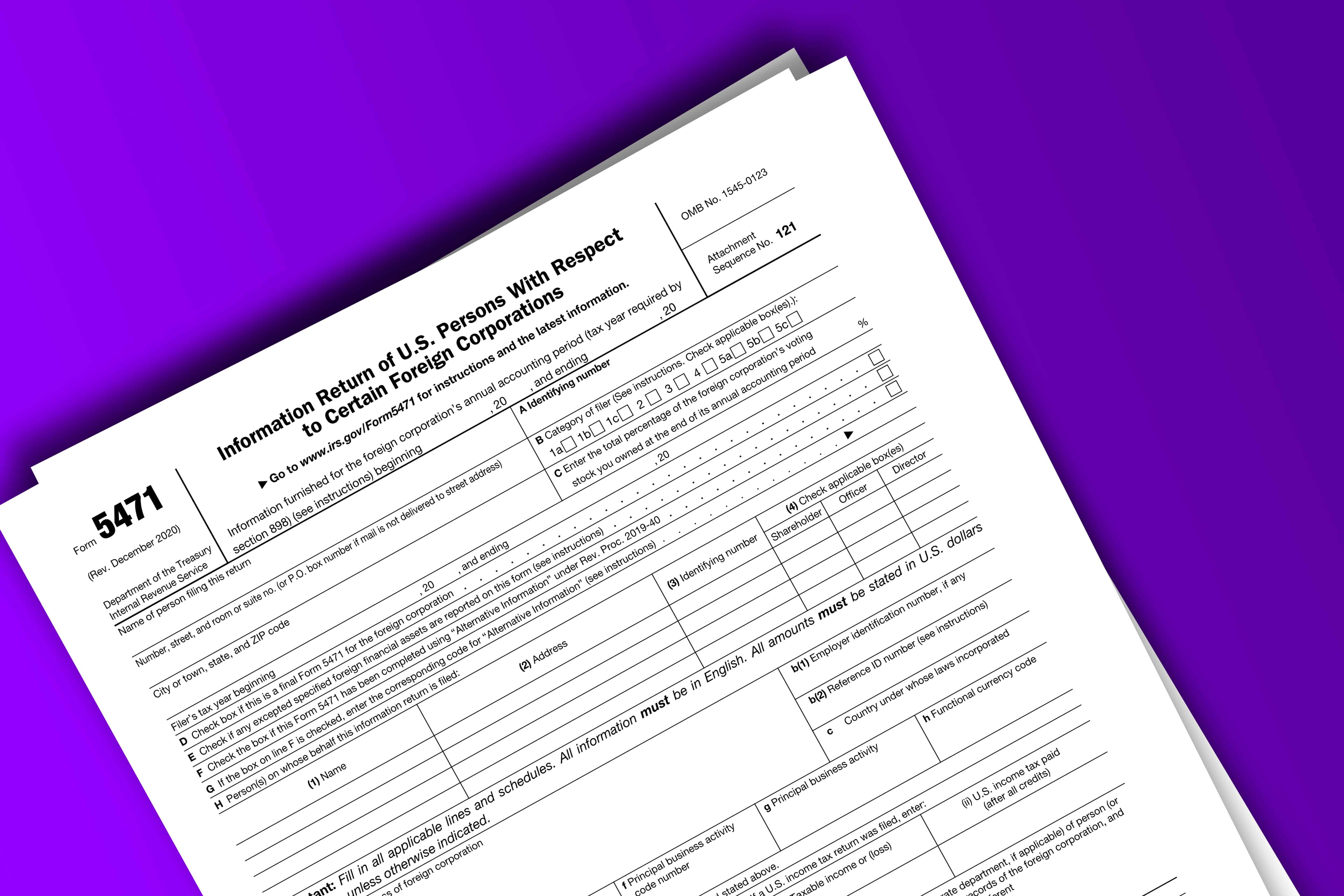

For each year at issue, the taxpayer was required to file Form 5471, Information Return of U.S. Persons With Respect to Certain Foreign Corporations, for each Belizean corporation, but he did not file the forms.

IRS’s Assertion of Form 5471 Penalties and Challenge in CDP Hearing

In 2016, the IRS mailed the taxpayer a notice of his failure to file the required Forms 5471 for the years at issue, but the taxpayer never filed them. For each year at issue, the taxpayer’s failure to file Form 5471 was willful and not due to reasonable cause.

In November 2018, the IRS assessed an initial penalty of $10,000 for each year at issue, and then a couple of weeks later, the IRS assessed continuation penalties of $50,000 for each year at issue.[2]

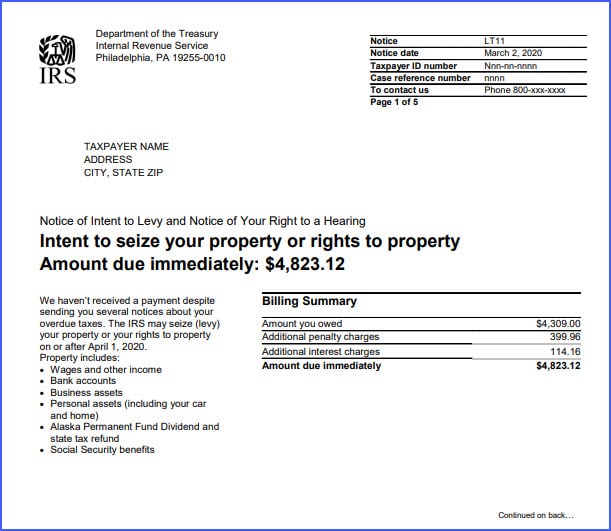

In January 2019, the IRS issued a Letter 1058, Final Notice of Intent to Levy and Notice of Your Right to a Hearing (levy notice) to allow enforced collection of the penalties. The taxpayer timely requested a collection due process (“CDP”) hearing pursuant. Since the taxpayer did not have a prior opportunity to dispute the penalties, the taxpayer was allowed to dispute the merits of the penalty. In his CDP hearing request, the taxpayer disputed whether the IRS has legal authority to assess section 6038 penalties.

Two and half years later, the IRS settlement officer issued a notice of determination. The settlement officer rejected the taxpayer’s challenge to the penalty and sustained the levy. The taxpayer then petitioned the U.S. Tax Court for a review of the notice of determination.

Tax Court Holds that IRS Does Not Have Authority to Assess Form 5471 Penalties

In the Tax Court litigation, the taxpayer and the IRS agreed that the only issue in dispute was whether or not the IRS has authority to assess Form 5471 penalties.

In Tax Court, the IRS and the taxpayer made technical, textualist arguments. The IRS argued that the term “assessable penalties” includes any penalties found in the Code that are not subject to the Code’s deficiency procedures. In addition, the IRS argued that the Code section enabling assessments of deficiencies was also broad enough to provide authority to assess any penalty in the Code.

The taxpayer argued that section 6038(b), unlike a number of other penalty sections, does not contain language authorizing the penalties it provides for. This, the taxpayer argued, leads to the conclusion that the IRS does not have the authority to assess the Form 5471 penalty. Instead, the government may only be collected through a civil action in a federal district court.

Judge Marvel weighed the textualist arguments and went through a deep, technical analysis of the text of the Code. Ultimately, Judge Marvel concluded that the constellation of the Code’s sections that enable the IRS to assess deficiencies (i.e., adjustments from examinations) and assessable penalties does not cover Form 5471 penalties. In addition, the Code section providing for Form 5471 penalties ( § 6038(b)) does not expressly provide authority to make assessments. As a result, Judge Marvel held that the IRS lacks statutory authority to assess Form 5471 penalties and may not proceed with enforced collection (i.e., levy) against the taxpayer.

IRS Appeals to D.C. Circuit

The IRS timely appealed to the D.C. Circuit. The IRS and the taxpayer again raised the same textualist arguments on appeal. However, the D.C. Circuit panel did not see the need to dive into the effectiveness of various interlocking Code provisions.

The D.C. Circuit acknowledged that § 6038 does not explicitly say whether Form 5471 penalties are assessable. The D.C. Circuit concluded:

“We need not embrace either party’s tax code-wide default rule to resolve this case. We accordingly do not pass on those broader theories beyond explaining why Farhy’s does not preclude assessment of section 6038(b) penalties. Instead, we conclude that a narrower set of inferences suffices to show that Congress intended to render those penalties assessable. Read in light of its text, structure, and function, section 6038 itself is best interpreted to render assessable the fixed-dollar monetary penalties subsection (b) authorizes. As a result, the Commissioner’s authority to assess all “assessable penalties” encompasses the authority to assess penalties imposed under section 6038(b).”

The remainder of the opinion explains the panel’s reading of the statutes and the inferences drawn that support its holding.

D.C. Circuit’s Holding Will Not Immediately Apply to All Taxpayers

Importance of the Golsen Rule and Venue on Appeal From CDP Hearing

Under the Golsen rule,[3] the Tax Court will follow its precedent unless the U.S. Court of Appeals to which an appeal would be made has already ruled on the issue. If an appeal lies with a circuit that has already ruled on the issue, the Tax Court will follow the precedent from the relevant court of appeals.

The IRS has treated Form 5471 penalties as assessable penalties and not subject to deficiency procedures. As a result, the IRS generally sends notification of the penalty on CP15, Notice of Penalty Charge.[4] These notices generally provide for an opportunity to challenge the penalty in a hearing with IRS Appeals.

However, sending a notice and demand for payment of the penalties starts the normal collection cycle. Eventually, the taxpayer will receive a notice with CDP hearing rights (i.e., LT11 or Letter 1058, Final Notice of Intent to Levy; Letter 3172, Notice of Federal Tax Lien Filing). These notices tend to come before the IRS Appeals hearing has concluded. Therefore, in many instances, the merits of the penalty are within the scope of a CDP hearing.

In Byers v. Commissioner,[5] the D.C. Circuit held that CDP hearing cases without a “redetermination” are appealable to the D.C. Circuit. However, if the CDP hearing case involves a “redetermination of tax,” then the standard rules of circuit court venue apply.[6] A challenge to the penalties is a redetermination of tax for this test.

Generally, in the case of an individual taxpayer seeking redetermination of a tax liability, a Tax Court decision may be reviewed by the court of appeals for the circuit of the taxpayer’s legal residence as of the date the petition for redetermination was filed with the Tax Court. However, if the individual’s legal residence is outside the United States, then the fall-back venue is the D.C. Circuit.[7]

For corporate taxpayers seeking a redetermination of tax liability, venue lies in the court for the circuit of the principal place of business or principal office or agency of the corporation, or, if it has no principal place of business or principal office or agency in any judicial circuit, then the office to which was made the return of the tax in respect of which the liability arises. However, if no return was filed, venue is then with D.C. Circuit.

If the taxpayer is an estate, venue lies in the court of appeals for the circuit of the legal residence of the executor, executrix, or representative of the estate, as of the date the petition was filed with the Tax Court.

The Tax Court opinion notes that Alon Farhy was a U.S. permanent resident for the years in question. However, in the appeal, the U.S. alleged that the taxpayer was a resident of Israel when he petitioned.[8]

For most U.S. residents, their appeal will not lie with the D.C. Circuit and the D.C. Circuit’s holding in Farhy will not be controlling. However, cased filed by non-residents as of the date of petition to U.S. Tax Court will be appealable to the D.C. Circuit and therefore the D.C. Circuit’s opinion in Farhy would control.

Could the Tax Court Change Its Opinion in Light of The D.C. Circuit Court Holding?

It is also possible that the Tax Court could decide to follow the D.C. Circuit’s holding in Farhy. The Tax Court may get a chance to revisit the issue soon.

Just a few weeks before the D.C. Circuit’s opinion, in Mukhi v. Commissioner, 162 T.C. No. 8 (April 9, 2024), the Tax Court followed its decision in Farhy. It held that the IRS did not have the authority to assess Form 5471 penalties. However, in the same case, the Tax Court sustained Form 3520 and Form 3520-A penalties totaling about $11 million. On May 10th, the taxpayer requested more time to file a motion for reconsideration.[9] The Mukhi case is appealable to the 8th Circuit Court of Appeals, so the D.C. Circuit’s holding in Farhy would not control. If the Tax Court reconsiders the case, it may have an opportunity to provide its stance in light of the D.C. Circuit’s opinion. Alternatively, if the case goes to the 8th Circuit on appeal, a separate circuit court could weigh in on the issue.

Conclusion

The D.C. Circuit’s holding is a significant win for the IRS. However, the battle over whether or not the IRS has the authority to assess Form 5471 penalties is not over yet. It will be interesting to see how the Tax Court reacts to the D.C. Circuit’s holding in the next Tax Court case involving the issue.

Notes

[1] See Farhy v. Commissioner, 160 T.C. No. 6 at 2 (2023).

[2] See IRC 6038(b)(1) and (b)(2) regarding the initial penalty and continuation penalties for failure to file Form 5471.

[3] See Golsen v. Commissioner, 54 T.C. 742 (1970), affd. 445 F.2d 985 (10th Cir. 1971), cert. denied 404 U.S. 940 (1971).

[4] A sample of CP 15 Notice can be found in the Internal Revenue Manual here: link to IRM. Alternatively, the IRS may assert the penalty on CP 215.

[5] Byers v. Commissioner, 740 F. 3d 668 (D.C. Cir. 2014).

[6] Code § 7482(a)(1) provides that U.S. Court’s of Appeal have jurisdiction to review Tax Court decisions:

“The United States Courts of Appeals (other than the United States Court of Appeals for the Federal Circuit) shall have exclusive jurisdiction to review the decisions of the Tax Court, except as provided in section 1254 of Title 28 of the United States Code, in the same manner and to the same extent as decisions of the district courts in civil actions tried without a jury; and the judgment of any such court shall be final, except that it shall be subject to review by the Supreme Court of the United States upon certiorari, in the manner provided in section 1254 of Title 28 of the United States Code.”

Section 7482(b)(1) (A) through (F). provides the rules for determining venue (i.e., which circuit court hears the case).

[7] See § 7482(b)(1):

“If for any reason no subparagraph of the preceding sentence applies, then such decisions may be reviewed by the Court of Appeals for the District of Columbia.”

[8] The Tax Court opinion noted that: “Unless otherwise agreed by the parties in writing, venue for an appeal would be the U.S. Court of Appeals for the District of Columbia Circuit. See § 7482(b)(1) (flush language).”Farhy v Commissioner, 160 T.C. No. 6

[9] For a deeper dive in the Mukhi case, see my recent post: Tax Court Rejects Excessive Fines Clause Argument and Upholds $11 Million Form 3520 and Form 3520-A Penalties