Magistrate Recommends Order to Compel Repatriation of Funds to Pay FBAR Penalties

Overview

A recent federal magistrate’s recommendation highlights a practical battle between the U.S. Government and a Defendant that is seeking to avoid payment of a $15+ million FBAR penalty: what happens if all of the defendant’s assets are outside of the United States?

In a federal suit to reduce the FBAR penalty to judgement, the Government successfully argued that the Defendant was liable for willful FBAR penalties for 2007, 2008, and 2009. However, the Defendant’s assets are all outside of the United States, so the Government could not garnish the Defendant’s assets to satisfy the liability. Therefore, the Government sought an exceptional remedy: an order to compel the Defendant to repatriate sufficient funds from Switzerland to the United States to pay the FBAR penalties.

On June 30, 2021, the magistrate agreed with the Government’s argument and recommended that the federal district court judge approve the Government’s request to issue a writ to compel the repatriation of funds to satisfy the liability.[1] It remains to be seen if the judge will adopt the magistrate’s recommendation.

Case Background

The Defendant was born in Germany and has lived in several countries including the US and Switzerland. The Defendant’s father was a successful businessman, who moved to Switzerland in the 1990’s. The Defendant’s ties to the US began in the 1990’s. He became a US resident in 1995 and a US citizen in 2000. In 2010 the Defendant moved and lived in Switzerland full time, but he came back to the US and lived in the US until sometime in 2019 or 2020.

While living in the United States, the Defendant maintained non-US bank accounts, but the Defendant did not file all necessary FBARs. The Defendant entered the OVDI Program but ultimate opted out of the program. Afterwards, the Government examined the Defendant’s tax returns and then assessed willful FBAR penalties against the taxpayer for tax years 2006, 2007, 2008, and 2009.

The Government then sought to reduce the assessment to judgement in Federal district court in order to enforce and collect the penalty. At trial, the Government successfully argued that the Defendant was liable for willful FBAR penalties for 3 years (2007, 2008, and 2009); the Court held that the Government did not meet his burden of proof for 2006.[2]

The Government then sought to collect the penalty from the Defendant. After entry of the final judgment, the Government sent the Defendant notices demanding full payment.

The Defendant did not voluntarily make any payment and did not respond to the initial demand letters.

In post-trial discovery, the Defendant confirmed “that he has no collection potential from assets in the United States because he moved them all offshore.”[3] All of the Defendant’s financial assets, including more than $49 million in banks, are outside the United States.[4]

The Government also learned that, after the court entered judgement, the Defendant sold his main asset in the US–a personal residence in Jupiter, Florida—and sent the funds to a foreign account.[5]

Through his counsel, Defendant has stated that he believes that, based upon the advice of Swiss counsel, his assets cannot be forcibly reached by the United States to satisfy the judgment.[6]

Then in June 2021, the Government sought a court order to compel the Defendant to repatriate sufficient assets to satisfy his FBAR penalty liability.

Since the United States sought a collection remedy pursuant to the Federal Debt Collection Procedures Act (“FDCPA”, Title 28 U.S.C. §§ 3001-3308), the Defendant was afforded a notice and an opportunity to be heard.[7]

Government’s Normal Collection Powers for FBAR Penalty Liabilities in the US

The Federal Debt Collection Procedures Act (28 U.S.C. §§ 3001-3308) provide the exclusive civil procedures for the United States to recover on an amount owed to the United States.

Under Section 3202[8], the United States may enforce a judgment by the enumerated remedies listed in Subchapter C (§§ 3201–3206). Generally, these remedies include (i) sale of property (Order of Sale or Writ of Execution); (ii) judgment lien against real property; (iii) garnishment of debtor’s wages or other property; (iv) installment payment orders; and (v) receivership.

In support of these remedies the United States may avail itself of any writ that a district court may issue under the All Writs Act (28 U.S.C. § 1651).[9] Writs are issued by a court after request from the government and usually after the debtor has had an opportunity to be heard. All property of the judgment debtor where there is a substantial nonexempt interest is subject to levy pursuant to a writ of execution.[10]

Property held by a third party is subject to a writ of garnishment if the debtor has a substantial non-exempt interest in the property. When the Government serves the writ on the holder of the property, the holder must turn the property over to the Government.[11]

However, courts only have an ability to issue writs on property within its jurisdiction. Therefore, a U.S. district court cannot issue a writ of garnishment to a debtor’s bank account in a foreign country (or even another state).[12]

All Writs Act and Extraordinary Remedies

Since the Defendant’s property is outside the United States, the Government is seeking the Court to issue an order to compel the Defendant to bring the funds back to the United States from Switzerland.

Government’s Legal Argument

The Government argues that the Court entered judgment in favor of the government and the Court has a variety of powers to enforce its judgement. However, the Government believes that it is unreasonable to expect that the Defendant will pay his liability since he has in essence “given up on the United States,” and “moved to Switzerland with no intent to return to the United States or to satisfy the judgment.”[13] And the Defendant has taken steps to render himself “judgment proof, which have rendered normal judgement collection tools (execution, garnishment, and levy) useless. Therefore, the Government is arguing that the Court must resort to an extraordinary power—order to compel repatriation of foreign assets–under the All Writs Act to enforce its judgment.

The Government pointed to other cases where courts have issued similar orders. However, none of those cases involved the enforced collection of a judgment related to FBAR penalties under Title 31.

The Government cites several cases to reinforce its argument that an order to compel repatriation is a proper remedy to collect FBAR liabilities. In United States v. McNulty, 446 F.Supp. 90 (N.D. Cal. 1978), the taxpayer failed to pay U.S. income tax on foreign sweepstakes winnings he deposited in a foreign bank account. The court in McNulty cited United States v. First National City Bank, 379 U.S. 378 (1965), in which the Supreme Court sustained a temporary injunction freezing the assets of a foreign corporation to prevent dissipation of assets. Also, in United States v. Ross, 196 F. Supp. 243 (S.D.N.Y. 1961), the taxpayer was subject to jeopardy assessments with respect to income tax liabilities. The government sought to freeze the taxpayer’s assets held in foreign countries, including the Bahamas. Since the court did not have power over the institutions holding the stock, the government sought to force the taxpayer to turn over the stock to a court-appointed receiver until the underlying liability could be litigated. The court in Ross ordered the taxpayer to transfer stock to a court-appointed receiver until the underlying litigation was resolved.

Defendant’s Argument

The Defendant raises several arguments as to why the Court should not grant the Government’s request for the repatriation order.

First, the Defendant points out that the District Court decision (i.e., the underlying substantive determination of whether or not the Defendant is subject to willful FBAR penalties) is still on appeal and therefore the order to force payment of liability is premature.

Second, the Defendant argues that the plain meaning of “repatriate” does not cover this case since Defendant’s assets came from and stayed in Switzerland. The Defendant provided the Merriam Webster’s definition of repatriate and notes that a vast majority of his assets never left Switzerland.[14] Further, the Defendant argues to the extent that he had money in the United States, specifically the proceeds from the sale of his house in Florida, those were subject to a state law homestead exemption and therefore those funds should not subject to execution.

Third, the Defendant notes that the case law cited by the Government for its request is distinguishable. Specifically, the cases cited by the Government are with respect to tax liabilities (under Title 26) or cases in which the Government is seeking to disgorge ill-gotten gains through the use of fraudulent or deceptive conduct (e.g., insider trading, fraudulent telemarketing scheme, etc). The Defendant argued that courts have more power to enforce a “disgorgement order” than they do a standard money judgment. Therefore, the attempt to collect an FBAR penalty under Title 31 is distinguishable from those cases.

After the Magistrate’s Report & Recommendation, the Defendant filed his Objections to the Magistrates Report & Recommendation.[15] In the Objection, the Defendant elaborates and stresses the argument that the All Writs Act does not provide “an independent collection remedy.” Instead, the FDCPA only incorporates the All Writs Act to assist with the enumerated remedies already in the FDCPA, which does not include an order to repatriate assets. Whereas in the cases cited by the Government, the orders to repatriate funds–to pay taxes or in relation to a jeopardy assessment–referenced a provision in the Internal Revenue Code (Title 26), which appears to authorize the use of a writs to enforce internal revenue law (including collection of tax).[16] However, that Internal Revenue Code Provision is not implicated in this case since the Government is seeking to collect FBAR penalties under Title 31.

Magistrate’s Determination

The Magistrate points out that the Court has authority to enforce the judgement and that it has all of the normal powers to enforce the judgment (e.g., garnishment). However, those powers are ineffective because the Court does not have direct power over the Defendant’s assets. Nevertheless, the Magistrate reasons that the Court has jurisdiction over the Defendant, so the Court has the power to order him to take action (i.e., repatriate funds) to enforce the Court’s judgement.

After exhausting the procedures specifically available under the FDCPA, a court may issue any writ necessary or appropriate to support a writ of garnishment. 28 U.S.C. § 3202(a) (citing the All Writs Act, 28 U.S.C. § 1651); see also Penn. Bureau of Corr. V. U.S. Marshals Serv., 474 U.S. 34, 43 (1985) (“The All Writs Act is a residual source of authority to issue writs that are not otherwise covered by statute.”). An order to repatriate funds is precisely the kind of order permitted by the All Writs Act. “Personal jurisdiction [gives] the court power to order [the defendant] to transfer property whether that property was within or without the limits of the court’s territorial jurisdiction.” Citronelle-Mobile Gathering, Inc. v. Watkins, 934 F.2d 1180, 1187 (11th Cir. 1991) (alteration in original) (quoting United States v. Ross, 302 F.2d 831, 834 (2d Cir. 1962)); see also, e.g., United States v. McNulty, 446 F. Supp. 90, 92 (N.D. Cal. 1978) (“It is clear, then, that this court, by virtue of its jurisdiction over the defendant, has the power to order him to repatriate the assets located in the foreign bank.”) (emphasis added).

Accordingly, a court[] has the authority to order a party under its jurisdiction to repatriate foreign assets when it is appropriate to support a writ of garnishment under the FDCPA.1 See United States v. Grant, No. 00-8986, 2005 WL 2671479, at *2 (S.D. Fla. Sep. 2, 2005) (J. Klein).

Magistrate’s Recommendation at 3.

The Magistrate also dismissed the Defendant’s argument that the Florida Homestead exemption shelters the proceeds from the sale of his home. The Magistrate points to the fact that the Government is not asking the Defendant to sell his home.

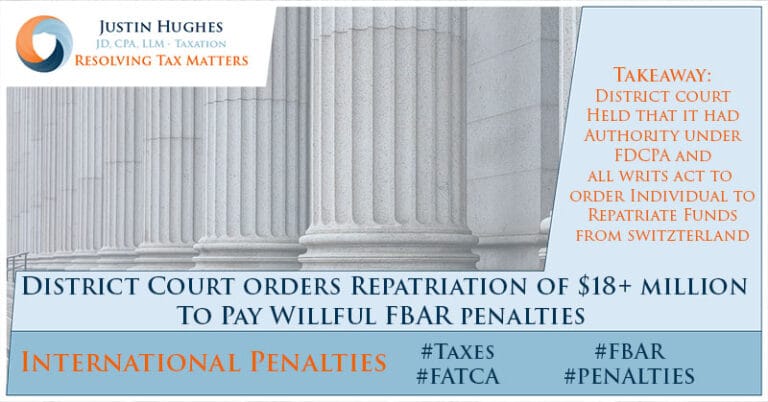

Therefore, the magistrate recommended that “the Court order [the Defendant] to repatriate $18,227,465.89, in addition to any additional post-judgment interest and penalties accrued since May 31, 2021.”

Utility of Court Order Against Defendant Outside US?

The Court is currently being asked to determine whether or not to issue the order. However, there has been no discussion of whether or not the order could be enforced if Defendant and his assets remain in Switzerland.

The Defendant has already asserted that, based upon the advice of Swiss counsel, he does not believe that he can be forced to move the funds back to the US to pay the FBAR penalties.

Enforcing judgments in another country’s court is generally not a simple or quick task. It remains to be seen if the Government would move to enforce the judgment in Switzerland and whether the Swiss courts would enforce the judgment.

What’s Next?

The District Court judge will have to decide whether or not to adopt the Magistrate’s recommendation after receiving the Defendant’s Objections and the Government’s response. Assuming it does adopt the Magistrate’s recommendation and the Court issues the order to compel repatriation of the funds, the Defendant seems to have indicated that he will not comply (at least not until his appeal is decided). If he does not, then it is not clear how the Government will attempt to leverage a US District Court order to force the Defendant to pay the FBAR penalty if the Defendant and his assets are in Switzerland.

Notes

[1] See Schwarzbaum v. US, No. 9:18-cv-81147, (S.D. FL. June 30, 2021) (Dkt No 124).

[2] The Defendant did not report all of his accounts based upon erroneous advice he received from his CPA in connection with the preparation of Defendant’s 2006 US federal income tax return. For 2006, the Court determined that the Defendant’s reliance on his tax preparer negated an inference of “willfulness”. With respect to 2006, the judge determined that the IRS could not prevail on the theory that the Defendant was imputed to have knowledge of the FBAR filing requirements simply by filing his federal income tax return with Schedule B attached to it. However, the Defendant self-prepared 2007, 2008, and 2009. The Court determined that after reading the FBAR instructions (i.e., FinCEN 114) the Defendant was aware or should have been aware that he had to report all of his foreign accounts. Therefore, the Court found that the Defendant was liable for FBAR penalties for 2006, 2007, and 2008.

[3] See Dkt 115 at 5.

[4] See Dkt 115 at 3.

[5] Dkt 115 at 3.

[6] See Dkt 115 at 3-4.

[7] See 28 U.S.C. § 3202(b)-(d),

[8] See 28 U.S.C. § 3202(a).

(a) Enforcement remedies.–A judgment may be enforced by any of the remedies set forth in this subchapter. A court may issue other writs pursuant to section 1651 of title 28, United States Code, as necessary to support such remedies, subject to rule 81(b) of the Federal Rules of Civil Procedure.

[9] 28 USC 1651(a)

(a) The Supreme Court and all courts established by Act of Congress may issue all writs necessary or appropriate in aid of their respective jurisdictions and agreeable to the usages and principles of law.

[10] See 28 U.S.C. § 3203(a) and (c); see also Fed. R. Civ. P. 69(a); United States v. Toll, Case No. 16-cv-60922, 2016 WL 4549689, at *4 n.2 (S.D. Fla. Sep. 1, 2016) (Bloom, J.).

[11] See 28 U.S.C. § 3205(a)-(b).

[12] See e.g., Stansell v. Revolutionary Armed Forces of Colombia (FARC), 149 F. Supp. 3d 1337, 1340-42 (M.D. Fla. 2015); Inversiones Y Procesadora Tropical Inprosta, S.A. v. Del Monte Int’l GMBH, Case No. 16024275, 2020 WL 6384878, at*4 (S.D. Fla. Aug. 5, 2020) (Louis, M. J.).

[13] Dkt 115 at 4.

[14] “Repatriate means “to restore or return to the country of origin, allegiance, or citizenship.” Repatriate Definition, Merriam-Webster.com, https://www.merriam-webster.com /dictionary/ repatriate (emphasis added)…. Simply stated, [Defendant] cannot repatriate funds to the United States when those funds never left Switzerland to begin with—a fact of which the government is keenly aware. [Defendant] did not transfer funds out of the United States to frustrate the government’s collection efforts as nearly all of his wealth has been held in Swiss banks since [Defendant]’s German/Swiss father deposited such funds in those same banks decades ago.” See 121 at 3

[15] 125

[16] IRC § 7402(a):

The district courts of the United States at the instance of the United States shall have such jurisdiction to make and issue in civil actions, writs and orders of injunction, and of ne exeat republica, orders appointing receivers, and such other orders and processes, and to render such judgments and decrees as may be necessary or appropriate for the enforcement of the internal revenue laws. The remedies hereby provided are in addition to and not exclusive of any and all other remedies of the United States in such courts or otherwise to enforce such laws. Section 7402(a).

One Comment

Comments are closed.